how to take a yield protocol to market?

(without bullshitting yourself or investors)

this is a case study style breakdown.

not “what yield protocols are”.

not “how defi works”.

you’re a founder.

you’re building a yield product.

you’re asking: how do i actually get this off the ground and make it investible?

this is the answer.

first: what kind of yield protocol are you, really?

before GTM, before TVL, before tokens.

you need to be honest about where the yield comes from.

everything else flows from this.

there are two buckets. no third one.

bucket 1: synthetic / onchain-native yield

yield comes from:

leverage

basis trades

delta-neutral strategies

rebalancing

aggregators

“strategy sauce”

smart contract plumbing

aka: magic internet money (even if it’s well engineered).

in this bucket:

nobody cares how clever it is

nobody cares about your architecture

nobody cares about your vision

they care about one thing:

how much do i make, and for how long?

that’s it.

bucket 2: yield backed by something offchain (RWA)

yield comes from:

credit

treasuries

real businesses

real cashflows

real-world risk

still, yield matters most.

but now there’s a second question:

why should i do this through you, and not directly?

this is where most RWA protocols die.

because they forget they’re not the asset.

they’re the intermediary.

the universal truth (for both buckets)

yield protocols live and die by TVL.

not users.

not followers.

not impressions.

TVL is:

your market signal

your investor signal

your survival metric

you can have:

great UX

clean contracts

clever strategies

and still never cross $2m TVL.

that’s the graveyard.

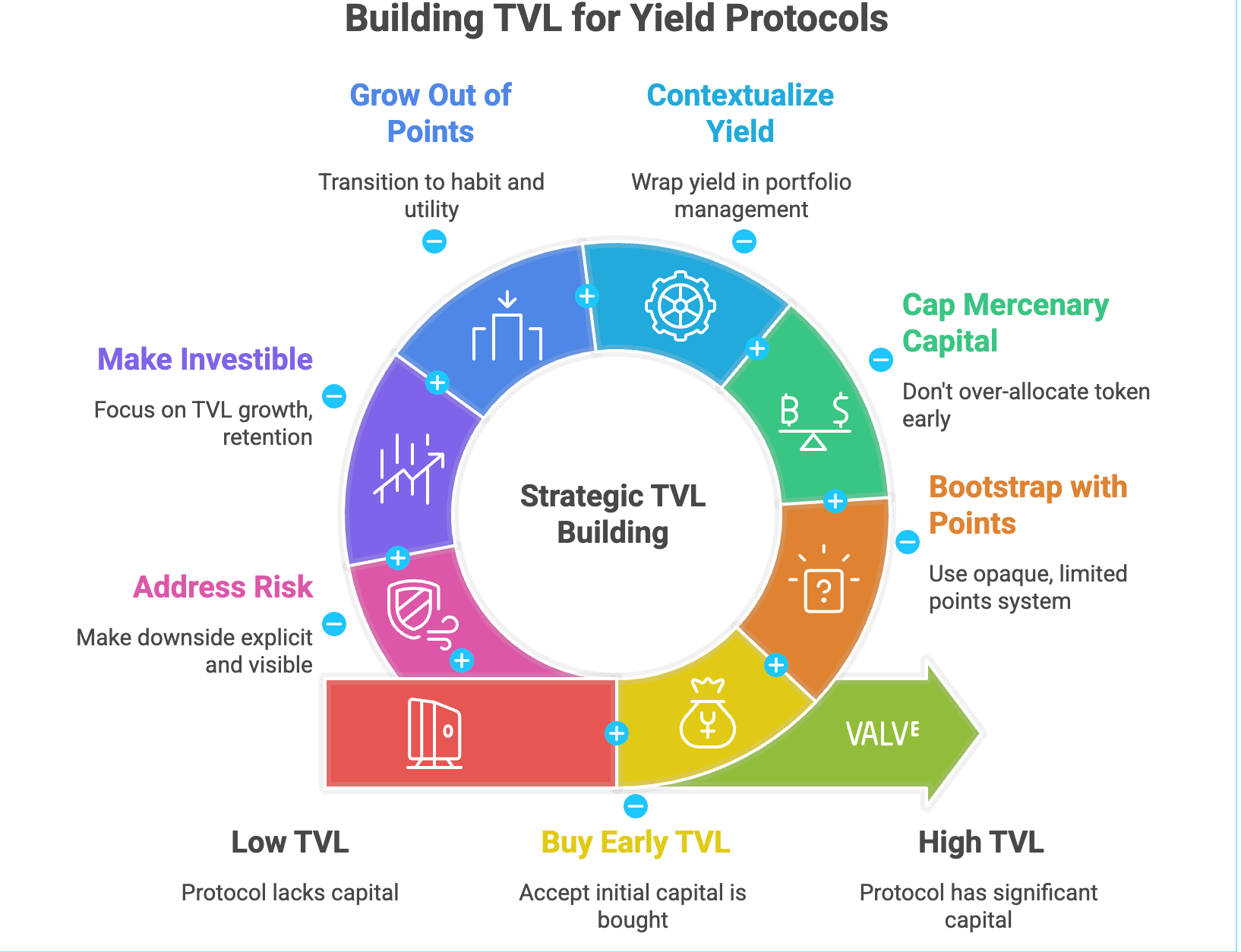

so how do you actually build TVL?

this is the sequence we’ve seen work.

not theory. practice.

step 1: accept that early TVL is bought, not earned

early TVL is not “organic”.

it comes from:

incentives

deals

private conversations

risk-reward asymmetry

pretending otherwise is cosplay.

the mistake is not using incentives.

the mistake is using them blindly.

step 2: decide what kind of capital you want

there are two types of money coming in early:

1) mercenary / institutional LPs

large checks

fast

ruthless

leave when incentives dry up

2) retail / long-tail users

smaller tickets

slower

sticky if narrative makes sense

your job is not to avoid mercenary capital.

your job is to cap it.

rule of thumb:

if >60-70% of your TVL can leave in a week, you don’t have TVL. you have a timer.

step 3: bootstrap TVL with a non-public points system

yes, points.

no, not the stupid version.

what works:

points only for LPs

no social tasks

no public leaderboard

no “post and earn”

no clear formula

rough guidance only:

“longer stays > more points”

“bigger capital > diminishing returns”

“early participation > bonus”

farmers optimize clarity.

remove clarity.

step 4: don’t blow your token allocation early

most yield protocols self-sabotage here.

common mistake:

massive points allocation

high implied FDV

token dumps at TGE

LPs leave

death spiral

early incentives should:

buy time

not define your entire cap table

if your protocol needs 30-40% of supply just to exist, it doesn’t work.

step 5: if you’re RWA, answer the real question

for RWA-backed yield, this matters more than APR.

investors and LPs will ask (explicitly or not):

why shouldn’t i do this deal myself?

your answer can’t be “because crypto”.

good answers look like:

access (they can’t get this deal otherwise)

aggregation (you bundle fragmented opportunities)

ops (you manage complexity they don’t want)

scale (ticket sizes don’t fit them individually)

speed (onchain rails beat legacy workflows)

bad answers look like:

vibes

“tokenization”

dashboards

buzzwords

you are selling convenience + access, not yield alone.

step 6: contextualize the yield

nobody wakes up thinking:

“i want yield”

they think:

“i want my money to work”

“i want stability”

“i want predictable income”

“i want exposure without headache”

successful yield protocols wrap yield inside:

portfolio management

treasury management

neobank-like UX

wealth tooling

specific narratives (real estate, credit, etc.)

yield is the engine.

context is the interface.

step 7: grow out of points, don’t stack them forever

points are scaffolding.

if you’re still dependent on them after:

6-9 months

product maturity

clear PMF signals

you have a problem.

long-term stickiness comes from:

habit

utility

reinvestment loops

trust

not emissions.

step 8: make it investible, not just fundable

fundable:

hype

trend

narrative

timing

investible:

TVL growth curve

capital composition

retention

yield sustainability

clear downside analysis

investors who matter will always ask:

“what happens if growth slows?”

you need an answer that’s not “we emit more”.

step 9: the risk question nobody wants to answer

“what happens if this breaks?”

for anyone deploying size, the real fear isn’t volatility.

it’s principal loss with no clear downside framework.

RWA-backed yield, credit-like structures, and anything touching real cashflows all carry real failure modes:

defaults

counterparties blowing up

legal or jurisdictional issues

hand-waving that away caps your TVL by design.

for example, @SpiceProtocol

is operating a shared coverage layers that let yield markets plug into a common protection standard, instead of everyone duct-taping their own solution.

the point is that if you’re building yield and you don’t make downside explicit and visible, your TVL ceiling is lower than you think.

either you build a real risk layer, or you integrate one early.

the real bottleneck

the hardest part is not:

contracts

audits

dashboards

it’s convincing people to park real money with you.

and they don’t do that because you’re clever.

they do it because the tradeoff makes sense.

TL;DR

yield protocols are judged on TVL, nothing else

first identify where your yield comes from

synthetic yield = pure numbers game

RWA yield = trust + access game

early TVL is bought, not earned

points can work if opaque and limited

mercenary capital must be capped

context beats raw APR

points are scaffolding, not a foundation

investible > fundable

this isn’t about being flashy.

it’s about not dying quietly at $1.8m TVL.

back to work.